Trump Wins, Yields Rise - What Does It Mean for Your Investments?

The Bottom Line:

A Trump presidency creates both risks and opportunities. Focus on domestic sectors, keep a defensive position in fixed income, and consider hedging strategies to protect against market swings.

Market Reaction to Trump’s Return

With Trump’s win, U.S. Treasury yields have surged, with the 10-year reaching 4.46% amid expectations of fiscal stimulus and deregulation. Equity markets have reacted positively, with S&P 500 futures up 2.3% and the Russell 2000 jumping 6%, as investors bet on a domestic-focused economic agenda. Meanwhile, a stronger dollar has pressured gold prices and weighed on international equities, especially in markets vulnerable to trade tensions and defense spending changes.

Key Implications for Global Trade, USD, and Oil:

- Trade Tensions: Renewed tariffs or restrictions on China could disrupt global supply chains, affecting multinationals and increasing market volatility.

- U.S. Dollar Strength: Initially supportive for importers, a stronger dollar may challenge exporters and firms with foreign revenues, especially if inflation expectations rise.

- Energy Markets: Trump’s pro-fossil-fuel stance and potential deregulation may boost U.S. oil production, pressuring global oil prices unless demand surges.

Impact on Equity Markets: U.S. and Global View:

Under Trump, sectors like energy, defense, and small caps may benefit, aligning with an “America First” agenda that prioritizes deregulation and domestic spending. In contrast, multinational companies with global operations, especially in tech and consumer goods, could face challenges from trade policies and a stronger dollar, which raises costs abroad. Emerging markets reliant on U.S. trade might also see heightened volatility.

Risks and Opportunities: Navigating This New Landscape

Key Risks:

- Rising Yields: Higher Treasury yields signal inflation risks, which could erode fixed-income returns.

- Trade-Related Volatility: Companies reliant on global supply chains, such as in tech and manufacturing, may face headwinds.

- Sectoral Shifts: Energy and traditional industries may gain, while renewable sectors could struggle.

Key Opportunities:

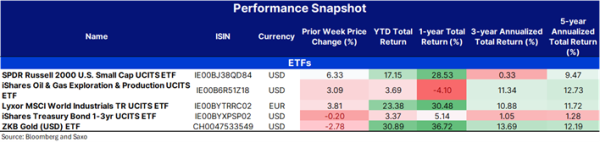

- Domestic-Focused Stocks: Small caps with U.S.-centric operations, like those in the SPDR Russell 2000 U.S. Small Cap UCITS ETF (R2US), could see benefits from pro-American policies.

- Energy Gains: Deregulation may boost fossil fuel stocks; investors might consider the iShares Oil & Gas Exploration & Production UCITS ETF (IOGP).

- Defense and Infrastructure: Defense spending and infrastructure investments could rise. For broad industrial exposure, the Lyxor MSCI World Industrials TR UCITS ETF (WIND) includes global aerospace and defense firms.

Strategies to Protect Your Portfolio:

- Diversify Across Asset Classes: Balancing stocks with bonds or real estate can offer stability. Rising bond yields suggest short-duration bonds, like the iShares Treasury Bond 1-3yr UCITS ETF (IBTA), may be more resilient.

- Hedge with Precious Metals: Gold remains a valuable long-term inflation hedge despite short-term USD strength. The ZKB Gold UCITS ETF (ZGLDUS) is a solid option for UCITS-compliant investors.