US inflation preview: Is it still too sticky?

What: US July inflation report

When: 12:30 GMT (14:30 CET) on Wednesday, 13 August 2024

Expectation: Headline CPI YoY 3.0% vs 3.0% (June) and Core CPI YoY 3.2% vs 3.3% (June)

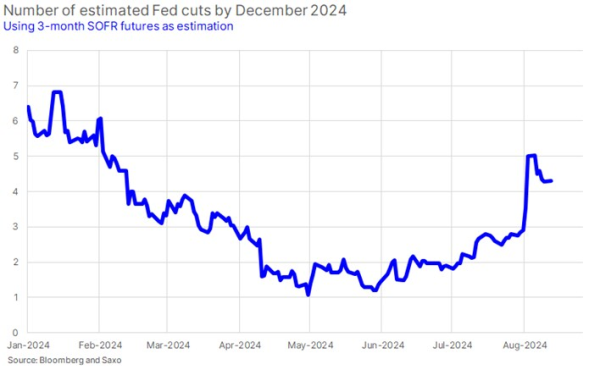

How will market likely react? Markets are likely to overreact to any inflation surprises due to low liquidity during the summer holidays. An upside inflation surprise could lead to reduced expectations for 100 basis points rate cuts by year-end currently priced into bond futures. Conversely, a downside surprise would solidify expectations for a 50 basis points rate cut in September and an aggressive interest rate cutting cycle ahead. Ahead of the FOMC rate decision in September, the move is more or less priced in 50/50 between either a 25 or 50 basis points rate cut.

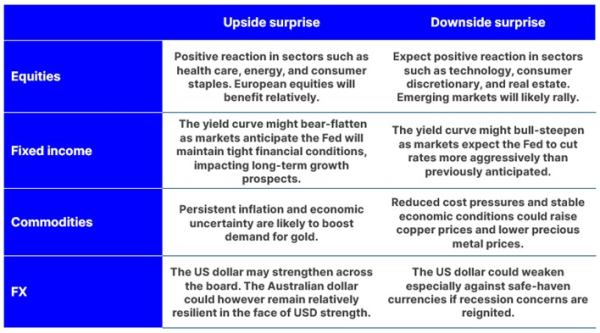

Below are potential market outcomes based on the US inflation report figures, considering both upside and downside surprises.

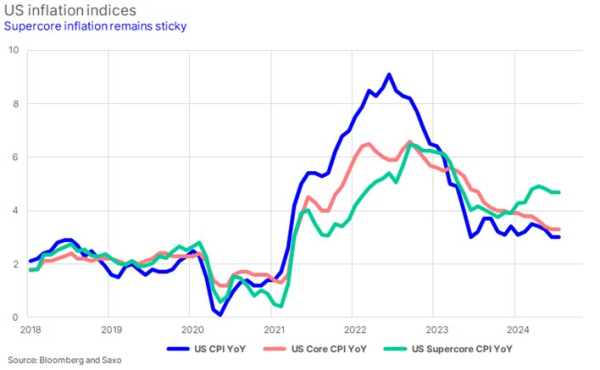

Why does it matter? For two years, US inflation reports have been key in influencing market expectations of Fed rate policies. Before the July meetings of the Federal Reserve and Bank of Japan, markets weren't anticipating even three rate cuts by year's end. However, the unwinding of the yen carry trade and a stock market crash led bond futures to price in up to five cuts by end of 2024. Despite declines in most inflation components since the peak in 2022, they remain above the 2% central bank target, with the “Supercore” inflation (measuring the least volatile items in the inflation basket) being stubbornly around the 4.5%.