US inflation report: How to trade the event

What: US March inflation report

When: 12:30 GMT (14:30 CET) on Wednesday, 10 April 2024

Expectation: CPI YoY 3.4% vs 3.2% (Feb) and core CPI YoY 3.7% vs 3.8% (Feb)

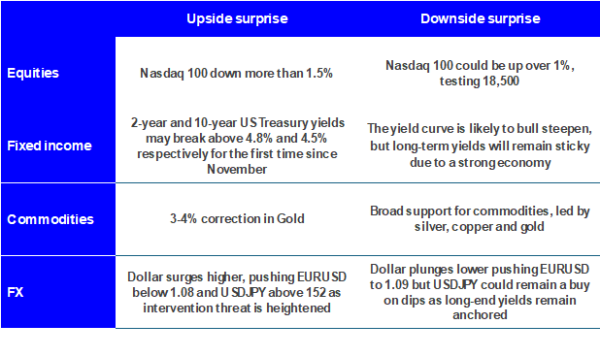

How will market likely react? US inflation has been running hot recently, with housing prices remaining sticky. Meanwhile, growth resilience from the US has prompted markets to push out Fed rate cut expectations, and just over two rate cuts are priced in for this year. Fed Chair Powell’s recent comments still suggest that he thinks the current inflation jump is a bump in the path of disinflation, and March CPI will be a key test of that narrative. If core CPI is higher than expected (upside surprise), then the reflation theme will gain more traction in markets. If core CPI is lower than expected (downside surprise) then markets can bring forward rate cut expectations back to price in the first full rate cut for June/July.

The below shows our views of market direction across key asset classes related to the US inflation report for both the upside and downside surprise outcomes.

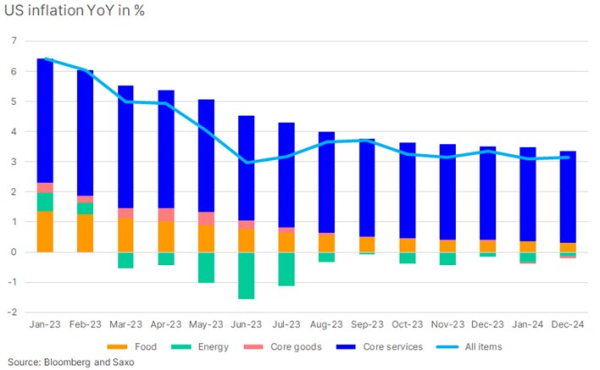

Why does it matter? US inflation reports have for two years been a key events impacting the market’s pricing of Fed’s policy rate. Earlier this year the market was pricing as many as seven US rate cuts, but recent inflation reports showing persistent inflation has caused the market to now only pricing in two and a half rate cuts by December this year. Some market participants are even beginning to talk about no rate cuts at all this year. As the chart below shows, all inflation components except core services have come down and this is the reason why the market will obsess about the core CPI rate.