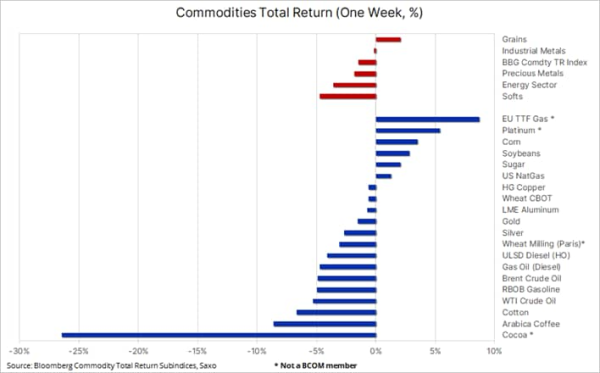

Weather-related boost to grains as softs and energy correction extends to a second week

Key points

- Commodity Sector Sentiment: Uncertain economic outlook, particularly in the US, leads to reversal of recent gains in commodity sectors, impacted by Federal Reserve's delicate balance between economic data and inflation concerns.

- Sector Performance Overview: Energy and precious metals sectors experience setbacks, while grains sector sees gains driven by weather conditions in key regions. Industrial metals pause amid signs of short-term softness in Chinese demand.

- Crude Oil Market Dynamics: Steepest weekly decline in oil prices in three months due to demand uncertainty and easing tensions in the Middle East. Long liquidation from hedge funds influences market movement, while OPEC+ expected to maintain production cuts amidst uncertain market conditions.

The commodity sector reversed some of the strong gains seen during the past two months after the general sentiment was weighed down by an uncertain economic outlook, not least in the US where the Federal Reserve needs to walk a tightrope between softening economic data, the latest example being April’s job report and continued price strength. Developments that for now support the prospect for US rates to stay “high for longer” due to persistent inflation, making the timing of the first, and potentially growth supportive rate cut highly uncertain, with the Federal Reserve possibly waiting until November post-election.

Most sectors tracked by the Bloomberg Commodity Index with the notable exception of grains traded lower led by the softs sector where cocoa slumped, with coffee and cotton following suit. The energy sector, apart from natural gas, suffered a broad setback with crude oil prices heading for their steepest weekly decline in three months on demand uncertainty, and easing tensions in the Middle East reducing supply risks. Precious metals traded lower for a second week, despite some emerging support from yen-led dollar weakness and lower bond yields following the dovish FOMC meeting and Friday’s weaker-than-expected US jobs report. Overall, however, gold continues to find support below USD 2,300 and has yet to challenge levels that may trigger a round of long liquidation from hedge funds.

The industrial metal sector surrendered some of their recent strong gains as the momentum-led rally showed signs of pausing amid data pointing to some short-term softness in Chinese demand for key commodities, not least copper. While there is little doubt the demand outlook for metals needed to support the energy transition remain strong and will likely lead to higher prices in the future, some short-term indicators point to relatively soft demand potentially raising the risk of profit taking and consolidation.

Finally, the grains sector traded higher for a second week with the BCOM Grains subindex reaching a three-month high, and while wheat consolidated following a 10% rally the previous week, corn and soybeans both traded higher on wet weather conditions across the US Midwest delaying planting, while Brazil and Argentina are dealing with dry and hot conditions in some areas and heavy flooding in Southern Brazil where one-third of the soybean crop remains unharvested. Developments that raise the risk of further price gains amid short covering from hedge funds that recently held a near record short position ahead of the Northern Hemisphere planting and growing season.

Copper focus turns to consolidation

In copper, the focus turned to consolidation with prices in London and New York trading lower after hitting two-year highs. Not least the USD 10,000 per ton level on the London Metal Exchange was seen as a level to book some profit following a very strong rally in recent weeks. Also attracting some attention are signs of softness in the short-term demand outlook in China where importers are paying the lowest premium over international prices in more than a decade while in London, the biggest contango between LME cash prices and the 3-month price point to soft demand as well. Combining these with the risk of long liquidation from hedge funds who amassed a major long position within the last couple of months, the short-term outlook points to consolidation.

Overall, we maintain a long-term positive outlook for the metal in anticipation of robust demand from among others towards electric vehicles, grid infrastructure and AI data centres at a time where production from existing miners looks set to fall in the coming years. A demand that will require higher prices in order to incentivise increased production from miners who in some cases are dealing with a twelve-year period of uncertainty between the discovery to the first metal being produced.

For now, support remains firm, and it would probably take a break below USD 4.41 per pound, the 0.382 Fibo retracement of the April rally, to trigger additional selling pressure from funds reducing long exposures.

Crude oil returns to an area of support

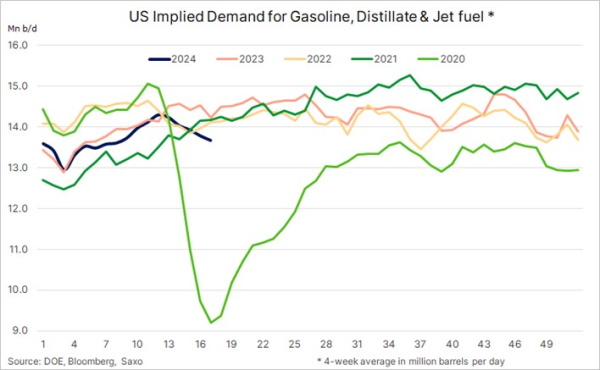

Oil prices are heading for their steepest weekly decline in three months on demand uncertainty, as rates are expected to stay higher for longer, and easing tensions in the Middle East reducing supply risks. The correction gathered some additional momentum on Wednesday after the US Energy Information Administration reported a rise in US crude stocks to a June high. While the increase was in line with seasonal trends it was another disappointing drop in implied gasoline demand to a 2020 low that caught the attention. Total demand for the three main fuels has seen a five-week decline to levels last seen in 2020 when the Covid-related shutdowns saw US and global demand temporarily collapse.

The mentioned weakness in some fuel markets, which includes China, and growing concerns the Federal Reserve may not deliver a demand boosting rate cut anytime soon as inflation remains sticky, together with an almost removal of the geo-political risk premium have all led to long liquidation from hedge funds, and they hold the key to how low the market may fall before support is reestablished.

Given Brent’s inability to build a base close to USD 90 per barrel, a minimum level sought by most of the OPEC+ producers, there is little doubt that the group will maintain current production cuts when they meet next month. Rolling back some of the cuts will require a tightening market through solid demand or through fading non-OPEC production growth, neither of which seems likely at this stage. From a pre-Houthi Red Sea attack low in December USD 72.29 per barrel to an April high at USD 92.18 per barrel, Brent crude has returned to trade near USD 83.00, the average price seen during this time, very much highlighting a crude oil market that will likely remain rangebound in the coming months.

Gold holds above key levels

Gold traded lower for a second week as the market continued to hold onto the bulk of the almost 450 dollars it rallied from the mid-February low. Two recent failed attempts to gain a foothold above USD 2,400 helped drive the current correction, but as data from the latest Commitment of Traders report showed, the near 3% correction in the week to April 28 triggered a small amount of net buying, not selling, and it highlights the strength of the rally with the bulk of the length (91.5k contracts or 285 tons) having been bought in early March below USD 2,200.

In other words, a much deeper correction is needed to trigger accelerated long liquidation. From a technical standpoint, the key area of support to watch in this regard is the USD 2,255-60 area where we find 61.8% of the March to April extension and 38.2% of the whole move from the mid-February low. Holding above this level will send a signal to the market that the retracement is nothing but a weak correction within a strong uptrend.We maintain our positive outlook for investment metals with the below drivers still the focus once the correction dust settles:

- Geopolitical risks related to an increasingly fragmented world

- Strong retail demand in China amid the desire to park money in a sector seen as relatively immune to a struggling economy amid deepening property woes and the risk of the Yuan weakness.

- Continued central bank demand amid geopolitical uncertainty and de-dollarisation, and not least gold’s ability to offer a level of security and stability that other assets may not provide.

- Rising debt-to-GDP ratios among major economies, not least in the US, raising some concerns about the quality of debt. In other words, rising Treasury yields are not necessarily negative for gold as they raise the focus on overall debt levels and the sustainability of those.

- In addition, the focus is changing from the negative impact of lower rate cut expectations towards support from a reaccelerating inflation outlook.

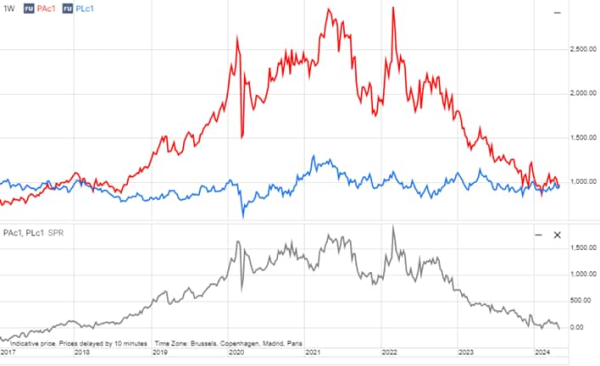

Platinum meanwhile was one of the best performing commodity this past week, rising more than 6% despite offering no technical buy signal as it remains stuck below key resistance near USD 1,000 per ounce. Instead the rally was most likely supported by forced short covering from hedge funds following another of several recent and now failed short selling attempts. In addition, the metal enjoyed support at the expense of palladium which returned to trade at the deepest discount to platinum since 2017, driven by a pessimistic outlook for demand from gasoline powered cars as the roll out of electric vehicles continues. Palladium is more exposed to that threat, with automakers making up 80% of demand for the precious metal, compared with 40% for platinum, according to figures from the World Platinum Council.

Commodity articles:

2 May 2024: Copper's momentum-fueled rally halts amid weakening fundamentals

26 April 2024: Commodity weekly: Sticky inflation and adverse weather focus

23 April 2024: What drives the gold and silver correction ?

19 April 2024: Commodity weekly focus on copper, gold, crude and diesel

17 April 2024: Copper rally extends to near two year high

16 April 2024: Crude oil's risk premium ebbs and flows

12 April 2024: Gold and silver surge at odds with other market developments

10 April 2024: Record breaking gold highlights silver and platinum's potential

5 April 2024: Commodity market sees broad gains, enjoying best week in nine months

4 April 2024: What's next as gold reaches USD 2,300

3 April 2024: Q2 Outlook: Is the correction over?

3 April 2024: Cocoa: A 50% farmgate price boost a step in the right direction

Previous "Commitment of Traders" articles

29 April 2024: COT: Gold bulls stand firm despite recent correction

22 April 2024: COT: Declining momentum may signal shift toward consolidation

15 April 2024: COT: Hedge funds propel multiple commodities positions beyond one-year highs

8 April 2024: COT: Speculative interest in metals and energy gain momentum

2 Apr 2024: COT: Gold and crude longs maintained amid strong underlying support