Week Ahead – A decisive week for USD with NFP and more; BoJ meets

- A crucial week lies ahead with US jobs report, advance GDP and PCE inflation

- The Bank of Japan is expected to hold rates, but will it flag a year-end hike?

- Flash GDP and CPI data for the euro area are also hotly anticipated

- Australian quarterly CPI and UK budget on the agenda too

All eyes on US data as Fed turns hawkish again

The Federal Reserve’s surprise decision in September to cut rates by a larger-than-expected 50-basis-points seems like a distant memory now, as policymakers are once again sending out hawkish soundbites.

US economic indicators since the September meeting have been on the strong side, including the CPI report, with Fed officials cautioning that another 50-bps cut is unlikely in the near term. The sudden switch in the narrative from ‘hard landing’ to ‘soft landing’, or possibly even a ‘no landing’, has spurred a sharp reversal in Treasury yields, which in turn has pushed the US dollar higher.

With the Fed’s November policy decision fast approaching, next week’s data will serve as a timely update on the strength of the US economy as well as on inflation.

Slowdown, what slowdown?

Kicking things off are the October consumer confidence index and the JOLTS job openings for September on Tuesday. But the top-tier releases do not start until Wednesday when the first estimate of third quarter GDP is due.

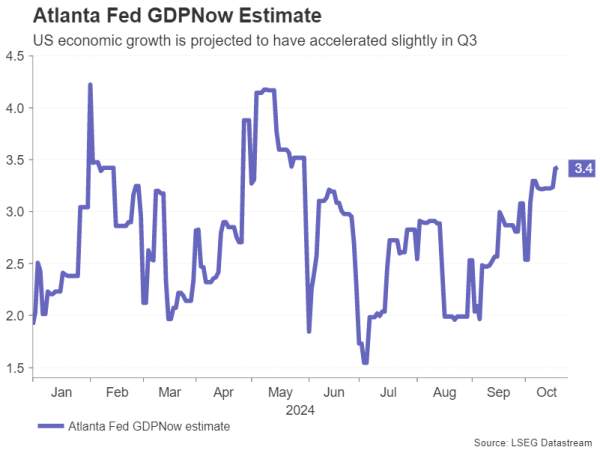

The US economy is expected to have expanded by an annualized rate of 3.0% in Q3, the same pace as in Q2. Not only is this above average growth but an upside surprise is more likely than a downside one as the Atlanta Fed’s GDPNow model puts the estimate at 3.4%.

Other data on Wednesday will include the ADP private employment report, which will provide an early glimpse into the labour market, and pending home sales.

Spotlight on PCE inflation after mixed CPI

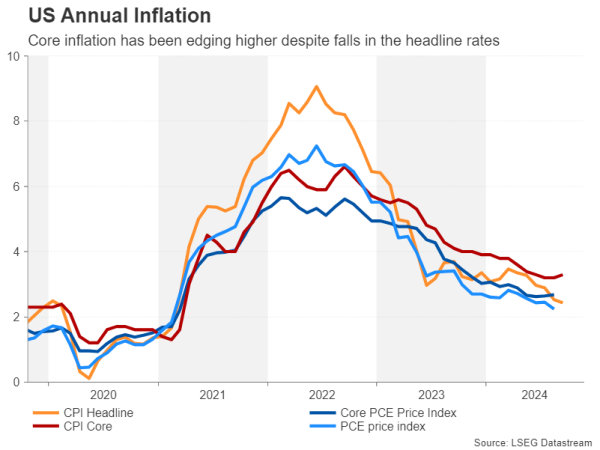

Both the CPI and PCE measures of inflation show a divergence between the headline and core readings. The core PCE price index, which the Fed puts the most weight on in its decision making, ticked up to 2.7% y/y in August even as headline PCE eased to 2.2%. It’s likely that both prints stayed unchanged in September or fell slightly. Hence, the inflation numbers may not be particularly helpful for the Fed or investors.

Still, the personal income and consumption figures due the same day will offer additional clues for policymakers, while October Challenger Layoffs and the quarterly employment cost will be watched too.

NFP report may hold the cards

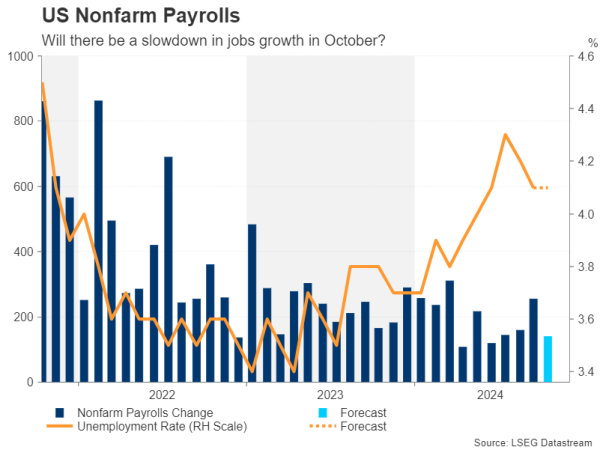

Finally on Friday, the week’s highlight – the October nonfarm payrolls report – will come to the fore. After a solid 254k rise in September, it’s projected that the US labour market created 140k new jobs in October, signalling a marked slowdown. Nevertheless, the unemployment rate is expected to have held at 4.1%, while average hourly earnings are forecast to have moderated slightly from 0.4% to 0.3% m/m.

Also important will be the ISM manufacturing PMI, which is expected to improve from 47.2 to 47.6 in October. With the Fed now more worried about the jobs market than inflation, soft payrolls could set the tone back to a more dovish one.

Can the US dollar extend its rebound?

Moreover, any signs that the American economy is cooling is likely to push up market bets of back-to-back rate cuts for the next few meetings. However, if growth remains robust and more significantly, PCE inflation points to some stickiness, rate cut bets will probably suffer a further blow.

At the moment, only one additional 25-bps reduction is fully priced in for 2024. If a rate cut in November starts to come into doubt, the US dollar could climb to fresh highs but stocks on Wall Street would probably come under selling pressure.

For the latter, however, a busy earnings week might keep the positive momentum going if results from Microsoft, Apple and Amazon.com don’t disappoint.

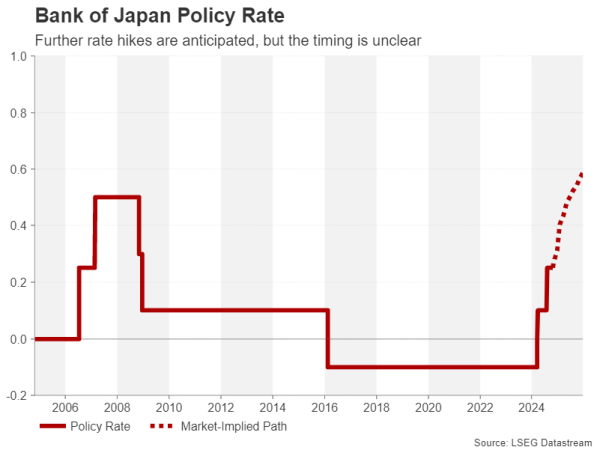

Bank of Japan expected to stand pat

Twenty twenty-four was a turning point for the Bank of Japan’s decades-long fight against deflation. The BoJ abandoned its yield-curve control policy, halved its bond purchases, and raised borrowing costs twice, ending its policy of negative interest rates.

However, despite policymakers’ clear intention to continue the normalization of monetary policy and raise rates even higher, inflation appears to be settling around the BoJ’s 2.0%, lessening the need for further tightening. The most recent commentary from Governor Ueda and other board members suggests a rate hike is not forthcoming on Thursday when the Bank announces its October decision.

But the updated outlook report with a fresh set of projections on inflation and growth should be quite insightful on the likelihood of a rate hike in December or during the first few months of 2025.

In the absence of any hints about a rate hike anytime soon, the yen will probably continue to struggle against the US dollar. Yet, a renewed weakness in the yen will only incentivize policymakers to hike sooner rather than later and this is a risk investors may be overlooking.

Also on the Japanese schedule are preliminary industrial output figures and retail sales figures for September, both due on Thursday.

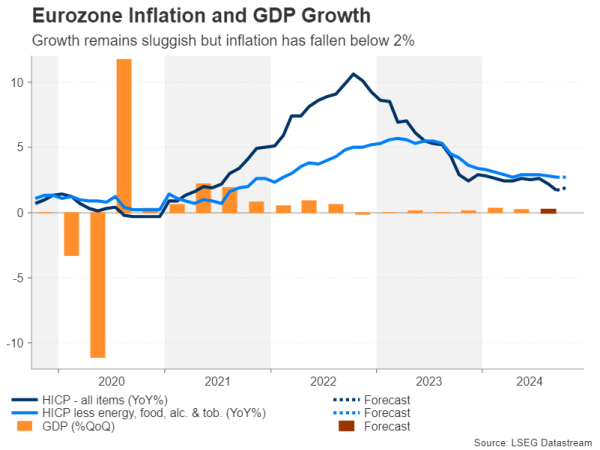

Euro awaits flash GDP and CPI

The euro’s double top pattern against the greenback did not let down technical analysis enthusiasts and the pair recently brushed 16-week lows, falling below $1.08. Next week’s releases are unlikely to be of much help to the bulls.

The flash estimate of GDP out on Wednesday is expected to show that the Eurozone economy eked out growth of just 0.2% q/q in the third quarter. On Thursday, attention will turn to the flash CPI readings. The headline rate probably edged up from 1.7% to 1.9% y/y in October, but the ECB is already forecasting a pickup in the coming months.

Nevertheless, stronger-than-expected data could provide the euro with some short-term relief following four consecutive weeks of losses. Alternatively, if the numbers disappoint, investors are sure to ramp up their bets of a 50-bps cut by the ECB in December.

Pound looking shaky ahead of UK budget

It hasn’t been the best of times for sterling either lately, despite the Bank of England being one of the more hawkish central banks at the moment. The pound has lost grip of the $1.30 handle, and there could be more downside on Wednesday when the UK Chancellor of the Exchequer Rachel Reeves announces the new Labour government’s first budget.

The UK press has gone into overdrive with its coverage of the budget and all indications are that Reeves will unveil tax increases of £40 billion, raising the tax burden to the highest since 1948. Whilst this may not be good news for taxpayers, BoE policymakers might welcome it, as tighter fiscal policy will dampen demand in the economy, paving the way for faster rate reductions.

The pound is at risk of slipping further from a deficit-reducing budget. Even if there are some growth boosting policies included, they are likely to be longer-term measures and not get in the way of the BoE cutting rates. Yet, there might be some support for sterling if investors take note of the fact that the UK government is focusing on long term investments and keeping the deficit in check rather than on short-term sweeteners for voters that push up borrowing.

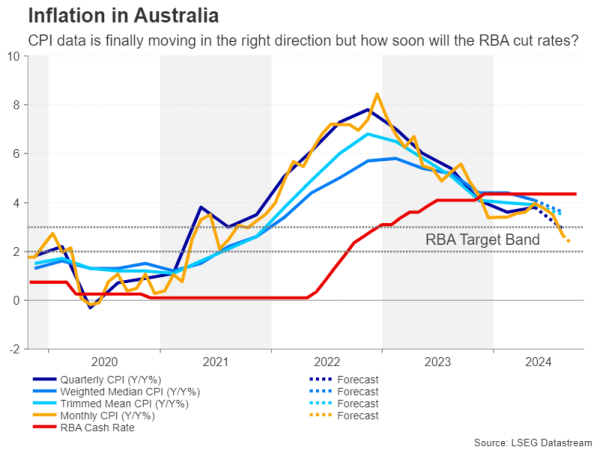

Australian CPI eyed as RBA decision looms

Finally, traders will be watching CPI stats out of Australia on Wednesday as the Reserve Bank of Australia maintains a neutral stance on rates. After edging up earlier in the year, inflation in Australia finally started moving in the right direction over the summer. The monthly print fell to 2.6% y/y in August, hitting the RBA’s 2-3% target band for the first time since 2021.

The quarterly data, which is deemed more accurate, is bound to form the basis of discussion for the November 5 meeting. However, even if there is more good progress in bringing inflation down, particularly in the trimmed and weighted mean measures, the RBA is likely to remain cautious for now and at best, begin the debate of when to start cutting rates.

But for the Australian dollar, a hawkish RBA may only go so far in coming to the aussie’s aid if broader market risk sentiment remains fragile and the US dollar stays strong. In addition to domestic data, aussie traders will also be monitoring China’s October PMIs out on Thursday and Friday.