Will the market get what it wants?

Key points

- Labour market focus: The Federal Reserve is gradually shifting its focus from inflation to the labour market, with the possibility of lowering its policy rate depending on upcoming labour market data.

- Interest rate expectations: Investors expect significant rate cuts by 2026, but the Fed may proceed cautiously, considering financial conditions and potential economic risks.

- Asset performance divergence: There is a significant performance gap between real estate stocks, which are benefiting from anticipated lower rates, and commodities, which are struggling due to weak demand from China.

It is all about the labour market

It has been made clear by several FOMC voting members that the Fed is gradually shifting its focus from inflation to the labour market. This means that the Fed, which was also indicated by Fed Chair Powell at the Jackson Hole event, is now in preparation for lowering its policy rate starting at the meeting on 18 September. The lower inflationary pressures in the economy allow room for lowering the policy rate. That is clear by now. The so-called “descent speed” will be determined by incoming data points on the labour market and in that regard this week is particularly interesting.

This week is the last batch of broad labour market data that the Fed will have on their hands before deciding on its policy rate later this month. At this point, the market is leaning in clear favour of a 25 basis point rate cut which seems appropriate given the current information picture. The broad labour market data such as the ADP employment change on Thursday and Nonfarm Payrolls on Friday are often lagging indicators confirming, or not, previous trends observed in other time series. The JOLTS job openings data on Wednesday is more interesting and a measure we know the Fed is looking at when analysing the US labour market.

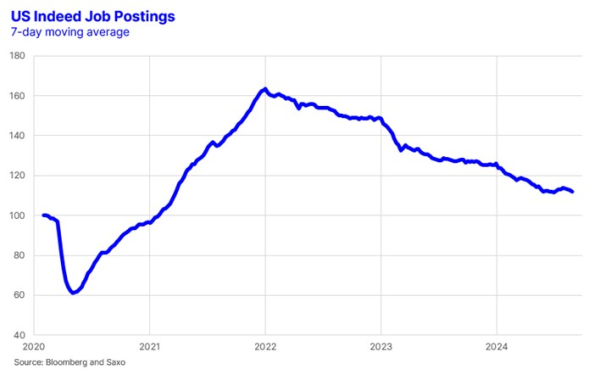

Job openings relative to the number of unemployed people in the economy is one measure of labour market tightness and well correlated with the subsequent wage pressures which again can explain inflationary pressures. This measure of labour market tightness is showing that tightness has eased the past two years to levels observed in the year ahead of the pandemic. If the labour market tightness stabilises at this level the Fed can go more slowly unless some external factor or other risk source hits the economy. The JOLTS data we get in two days is for July and thus this time series is lagging by one month. If one wants a faster weekly series the US Indeed job postings data is more timely. Here we see basically the same trend some indications of stabilization although this picture can quickly change.

Investors are getting more sure about lower interest rates

The market is convinced that the Fed will move its policy rate lower by 225 basis points by January 2026 reaching the proximate neutral rate. However, the economy is still exhibiting trend growth at around 2% real GDP growth. That is of course no guarantee for a recession not coming soon as the economy was also growing close to trend growth when the US recession officially started in December 2007. It confirms that the Fed is more confident that inflation is reasonably under control. The big question is how much pent-up demand there is stored in the interest rate parts of the economy. This is one of the reasons why the Fed might go slow in the beginning to see how the economy reacts.

Another way of looking at the coming rate cycle is through the lens of financial conditions. These measure how easy it is to obtain financing and refinancing of debt. Financial conditions adjusted for the strength of the economy are right at the average since early 2010 and quite loose in a longer historical context. Financial conditions were at higher levels and deteriorating in all rate cut cycles since early 1990 except for the rate cut in 2019. Financial conditions were a lot tighter in the period 1971-1984 when the Fed was battling inflation back then, and compared to today it could be risky for the Fed to move too aggressively.

The market wants significantly lower interest rates and it will for sure get it, but the speed and depth of interest rate cuts are still very uncertain. Also because the US election in November could be an important factor for the economy in 2025 and beyond. More updates on the US 2024 election and the different scenarios read our analyses on our US election page.

Commodities and real estate are two different worlds right now

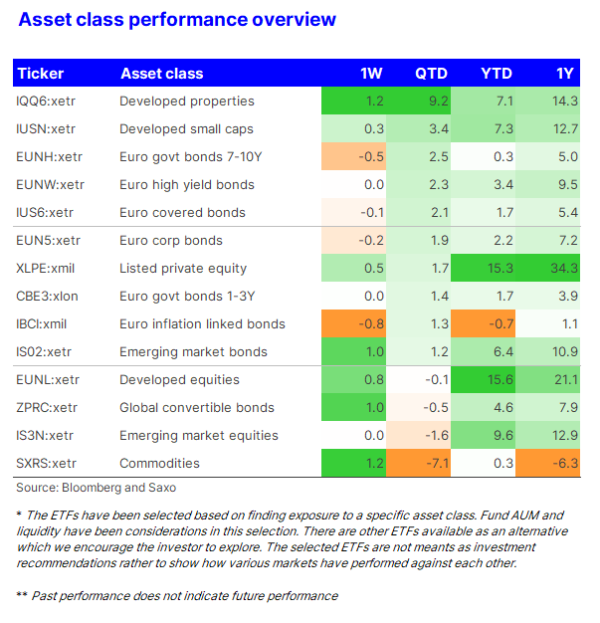

It has been a while since we have covered the macroeconomy and asset allocation. As the table below shows, this quarter has been very unusual in the sense that we are observing a very wide spread in performance between real estate stocks (+9.2%) and commodities (-7.1%). The stories driving this spread are the market’s narrative of substantially lower policy rates over the next 16 months and a weak China impacting demand for commodities.

As we have recently shown in our expected returns table on sectors, the real estate sector is still the least attractive given that the sector is still raising equity capital to fund itself which is negative from a shareholder perspective. One thing is lower policy rates, but if the long-term inflation premium remains sticky then the lower policy rate will only lead to a flattening yield curve and not substantially lower long-term financing yields which are what the real estate sector needs.

Commodities have staged a comeback through August, but the weakness coming out of China continues to be a drag on the overall commodities sector. We are still positive on commodities longer term as India will increasingly play a positive role on marginal demand as the country urbanises. The green transformation in the developed world will also continue to be positive for metals such as aluminum and copper.

Previous notes on asset allocation and macro

- The perfect storm hits market and what comes next (5 August 2024)

- Everyone on Wall Street is talking about these key risks (9 July 2024)

- French election: Is this a new Meloni moment for Europe? (24 June 2024)

- US rate cut seems distant as inflation report looms (10 June 2024)

- Commodities setback, investment drought in mining, and EM elections (3 June 2024)

- The inflation conundrum and private equity party (27 May 2024)